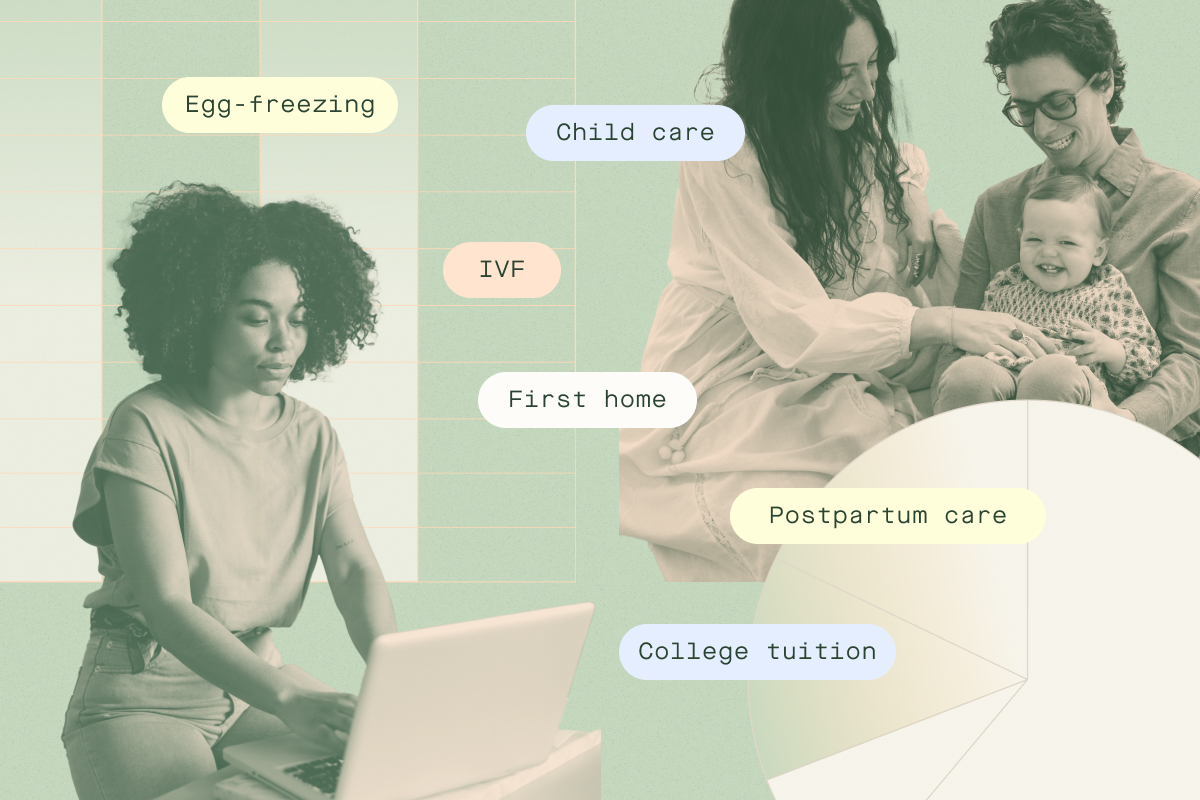

10 Top Financial Questions About Family Building

Starting a family, no matter what that looks like for you, costs women a lot. Learn how to prepare for a baby financially with the answers to family-building FAQs.

Starting a family, no matter what that looks like for you, costs women a lot. And not just financially. The effects on the body and mind from the process of becoming a mother are a whole other thing. Shockingly, this all gets overlooked in our society (that’s momwashing for you).

The all-women team of financial experts at Ellevest know this professionally — and those who are also moms know firsthand, too. That’s why we’re answering the 10 most-asked financial questions about family building: to help you lighten your mental load and feel more prepared when it comes to financial planning for starting a family.

Of course, the answers to these family-building questions will vary depending on your unique situation — where you live, what life stage you’re in, what your career looks like, and what your timeline looks like. But one tip that applies to anyone at any stage of the family-building process is to be as realistic as possible about the cost of having a family.

Use this Q&A to see what that means for you, so you can get a better idea of your financial options as you navigate how to best build your family. You can also watch a recording of our Family Planning Q&A with Maven Clinic, here.

- When should I start saving to build a family?

We can tell you this: No client our team has ever worked with has said, “I could have waited longer to start saving.” If family building is something you’re thinking about now, start saving what you can now. If it’s something that’s going to be your reality soon — maybe you want to freeze your eggs fast or you experience an unplanned pregnancy — start saving what you can now.

- How much do I need to start a family?

Family-building numbers are big — bigger than many people imagine. But knowing these amounts is the first step to our top money tip for starting a family: Be as realistic as possible . We’ll break this down:

- It currently costs US parents roughly $300,000 to raise a child from birth to age 18 (not including higher education). That amounts to just over $16,000 a year … per child.

- The median household income is ~$75,000 before taxes. If you live in a major city — say New York or San Francisco — you’re probably paying 20% all-in for taxes. That $75,000 income became $60,000 pretty quickly.

- Now the conversation is: Where does that extra ~25% of income for starting a family come from? Is it already baked into your income or not? After swapping in their own income after taxes, the answer for many women is it’s not.

Do you dial back your expenditures by making lifestyle changes? Reroute retirement savings or money for other long-term savings goals? Ramp up your earnings capacity by taking a promotion or a consulting opportunity? Change your living situation to be closer to family for built-in support? These are all deeply personal questions that only you can answer … and they can be answered more confidently with a financial plan.

Since a good financial plan prioritizes all of your financial goals — including starting a family — it can help you make clearer money decisions driven by your core values and data, not by anxiety and pressure.

- How much can I expect my insurance and employer to cover?

Go straight to the source with these tips:

Health insurance coverage for family building:

- Ask for a written explanation of your benefits. Information tends to vary from person to person over the phone. For accuracy, request a copy of your plan.

- Calculate out-of-pocket expenses vs going through your provider. In some cases, things like medications can be cheaper out of pocket than sending a claim to your health insurance provider. It’s worth crunching the numbers.

- Determine your fertility benefits coverage. Fertility benefits are typically structured in two ways: up to a lifetime maximum dollar amount or up to a certain number of cycles / rounds. Find out which you have and what fertility-related treatments may require preauthorization from your insurance provider.

- Ask if there are restrictions on accessing your fertility benefits. Restrictions are often in place that require you to have a diagnosis of infertility to access fertility options like IVF, and may vary depending on what state you live in.

- Know what’s a qualified medical expense for FSAs / HSAs. Pretax contributions to these medical savings accounts reduce your taxable income (good!), but they need to be used for goods and services that are medically necessary. Currently, IVF is a qualified expense . For egg freezing, you’ll likely need a letter of medical necessity from your doctor (lifestyle or career reasons won’t cut it).

Employer-sponsored benefits for family building:

- Talk to your employer. For small companies, your Head of People should be a good person to tap first. For big companies, you might have a Director or VP of Benefits to go to. These people are the most knowledgeable about how your company’s benefits work and can help you get a better understanding of what’s offered through your health plan.

- Be aware of holistic health and wellness resources offered. Does your company offer special access to mental health services? Medical clinics? Career coaching? These resources can also be a big support to you during this time.

- Seek out employee resource groups (ERGs). Community matters for people wanting to become parents. See if you can be connected to ERGs that normalize talking about family building.

- How do I talk about this with my employer?

We’ll state the obvious: The workplace can be a hard place for women, especially moms. That makes many women in the workforce afraid to tell their boss that they’re pregnant. To feel less stressed about the inevitable talk, take time to review and understand your workplace rights and company policies.

Next, consider how you think your news will be received. Are pregnancy and parenthood accepted at your workplace? Or are they supported and celebrated? How have your co-workers’ pregnancies affected workplace culture in the past? If you’re the first person at your workplace to become pregnant, you may want to set up a time to tell your boss in person or on a video call so you’re face-to-face. It’s OK to wait to tell your boss until after a performance review or big project ends (if it makes you feel better and if you have the time). If it’s not well received, reach out to your HR contact.

All of this is an unfair amount of pressure to place on pregnant people. But there’s good news: Employer benefits for parental leave and family planning are transitioning from nice-to-haves to need-to-haves. According to one report, 75% of employers surveyed say reproductive and family benefits are important for retaining employees. Additionally, 48% of employers surveyed plan to increase their family health benefit offerings in the next two to three years.

- What if I’m self-employed?

Variable compensation makes having a strong financial base a good idea in general. It’s ideal for anyone who wants to become pregnant to be as financially sound as you can be. That means building a strong financial foundation, including having a healthy emergency fund, before you start saving for building a family.

That can be a hard truth for people wanting to become pregnant to hear. It’s common for our clients — self-employed or not — to share, “I’ll do anything to start a family.” But we strongly encourage them (and you) to “put your oxygen mask on first.” A financial plan can help you navigate what to do and how to stay on track with family-building goals in relation to your short- and long-term goals — you don’t necessarily have to give up on other goals to get the family you want.

Community is equally crucial for people who are self-employed. Sign up for local or online groups that can give you firsthand support with starting a family.

- How should I start saving to build a family?

The first step for saving to build a family is to talk about it. Talk about money, talk about goals, talk about reality. These conversations can inform your next considerations. Besides more obvious considerations (think: how much will it cost us?), don’t overlook topics like renting vs buying a home, upsizing or upgrading your current space and vehicles, or moving closer to family or not.

- How do I make the most of my family-building savings?

Keep family-building savings separate from other accounts for visibility and ease. Park your money in an NCUA- or a FDIC-insured high-yield savings account to take advantage of the higher interest than typical savings accounts offer.

- Should I invest for family building?

Many clients start investment accounts like 529s, Roth IRAs, and trusts to help pay for their kids’ education. But many clients who have time to invest for family building don’t. Like any long-term goal, investing toward it is a good idea.

For example, the current cost for one round of egg freezing is $15,000. If you started investing $100 a month toward that goal during your 20s or 30s, you’d probably meet the cost in 10 years, no problem.

- How does financial planning change for things like egg freezing, IVF, and surrogacy?

One in six people worldwide struggle with infertility. Overall, there are different costs to think about depending on which route you take … that is, if fertility treatment is the right and best step for you at this stage.

According to our friends at Maven, the world’s largest virtual clinic for women and families, there’s lots of pressure for women in their mid-30s to pursue fertility treatment as a first step to pregnancy. Of course, there are challenges to conceiving naturally as you age. But, according to Maven, if natural conception is an opportunity, take it. From a financial standpoint, we agree.

Here’s a quick overview of fertility treatment costs:

Egg freezing costs

- $10k–$15k per cycle (most women require multiple rounds)

- $300–$1k per year for storage (most women require between 3–6 years)

- $3k–$11k for additional medications

IVF costs

- $15k–$30k per cycle (most women require multiple rounds)

Surrogacy costs

- $150k–$200k all in

For those looking to adopt, here’s a quick cost overview:

Adoption costs

- $30k–$60k for domestic adoption via private agencies

- $20k–$50k for international adoption via private agencies

- ~$3k for adopting a child from foster care or foster-to-adopt

- Are there any tax benefits or deductions available for fertility treatment expenses?

So much of the answer to this depends on the Internal Revenue Service (IRS), our governing federal tax authority. And that’s because HSA / FSA usage and tax deductions tie back to this idea of “qualified medical expenses.” Fertility treatments such as in vitro fertilization (IVF), fertility medications, and other assisted reproductive technologies may qualify as medical expenses for tax deduction purposes. If a fertility procedure is carried out for non-medical reasons, eligibility becomes fuzzier.

As highlighted in some of these answers, we understand that planning for a family involves navigating a variety of financial considerations. Ellevest can support you with that — and in more ways, too. Our all-women team of financial experts are here to meet you where you are and help you work toward your financial goals in whatever form fits your schedule and budget the best.

About Ellevest

Founded in 2014, Ellevest is a women-founded, women-led financial services company dedicated to closing the gender wealth gap. Our mission is to get more money in the hands of women, their families, and the next generation through personalized, intentional wealth management, and financial planning.