Monthly Market Insights: Are Stock Prices Too High?

Sticky inflation. Higher interest rates for longer. And the very, very long runway of economic potential for advanced technology and AI.

After a resounding strong start to the year, markets pulled back in April, with the S&P 500 ending the month down 4.2%, the DJIA down 5%, and the NASDAQ down 4.4%. All of the factors that fueled Q1’s market rally — optimism around a soft landing, inflation that would continue to ease downwards, and the anticipation of interest rate cuts in 2024 — are now in question.

The latest inflation data shows the personal consumption expenditures index (PCE, the Federal Reserve’s preferred inflation gauge) rising 2.7%, a slight jump from the month before, and still a ways off from the Fed’s 2% target. Experts who previously forecasted six rate cuts in 2024 have pared that prediction back to just one or two, with some believing that a rate increase could even be possible. Just this week, Fed officials indicated they'll hold rates steady for the foreseeable future.

The culprit in this conundrum? Stubborn inflation.

It isn’t budging as much or as quickly as expected. Why? Everything from sustained high housing costs, rising oil prices that are impacting the cost of gas, excessive government spending, increasing wage growth, and robust consumer spending — which helps keep the economy humming, but also drives up demand and, by extension, prices.

With sticky inflation comes interest rates that will remain higher for longer, creating a less favorable environment for both stocks and bonds. The yield on the benchmark 10-year US Treasury ended the month at 4.67%, narrowing the gap between stock and bond yields (more on this later).

Even with markets pulling back last month, many believe stock valuations are still too lofty, given an uncertain outlook and the high likelihood that rates will remain at current levels for the foreseeable future. Market analysts often look at measures such as the price-earnings ratio (“P/E ratio”) or Shiller’s cyclically adjusted version of this metric (“CAPE ratio”). The chart below shows the CAPE ratio of the S&P 500, defined as the S&P 500 price index divided by the inflation-adjusted average earnings from the prior ten years. At 34.4x, it far exceeds recent as well as historical averages. However, it’s not the highest it's ever been.

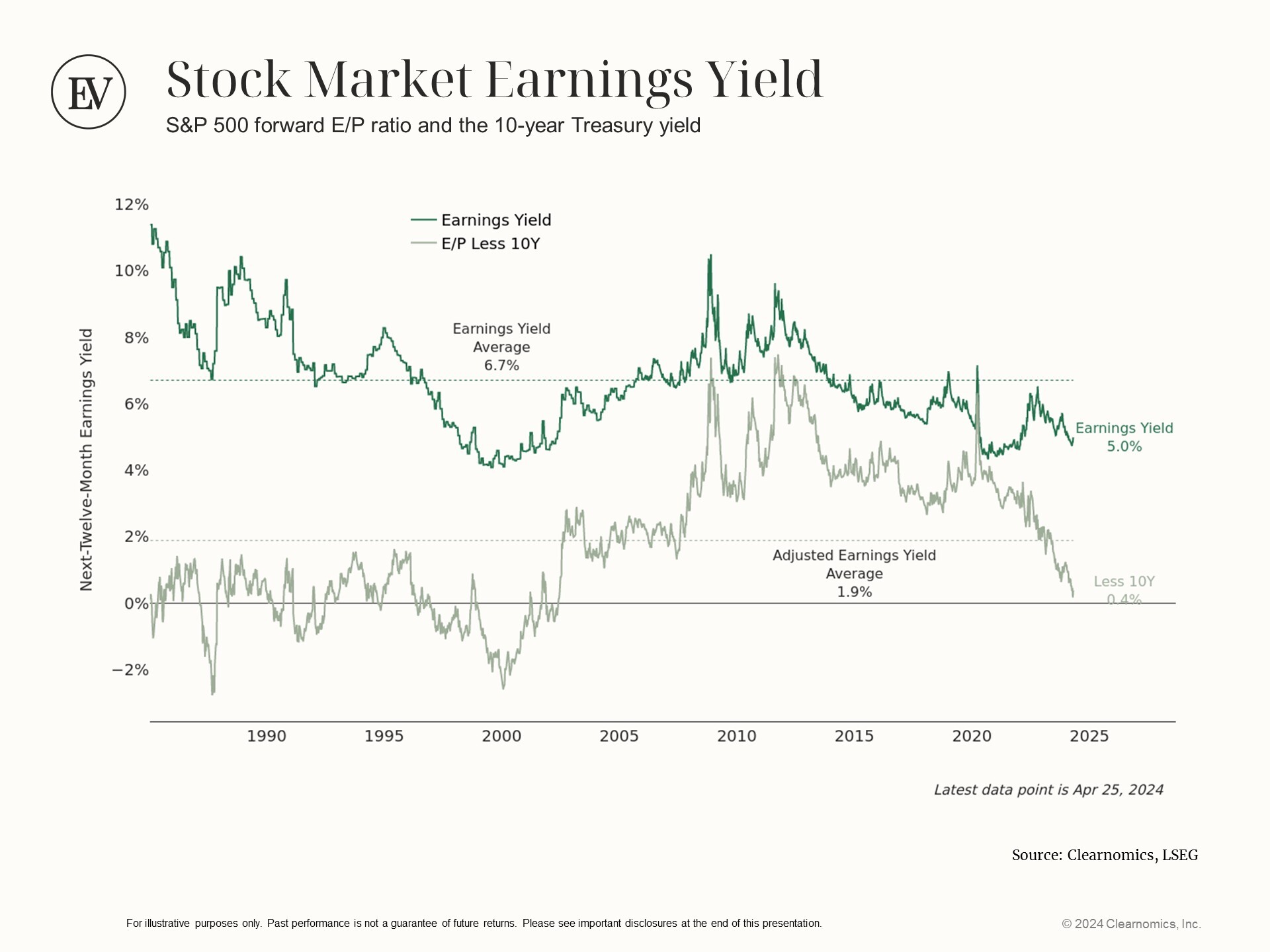

Another measure of valuation compares the earnings yield of the stock market and that of the 10-year US Treasury. The greater the difference between these two yields, the more investors are compensated for taking equity risk. The chart below shows how far the stock market’s earnings yield has fallen as markets have rallied. At the same time, the yield of the 10-year US Treasury has risen, such that the extra yield for investing in stocks relative to US Treasuries is close to zero. Of course, this comparison isn’t apples-to-apples, since the value of equities has the potential to grow (or shrink) — whereas the principal value of US Treasuries is fixed.

Based on these two measures, the CAPE ratio and earnings yield, stock prices today appear rich compared to history. But can these high prices be justified? Will future earnings growth be robust enough to support these prices? In a world of rate cuts, possibly. Easing inflation and lower rates will help, but there’s another factor that could fuel earnings and provide justification for higher prices.

And that’s the impact of innovation.

While many fear the loss of jobs to advanced technology and AI robots, so far, those fears have been overblown. A number of companies investing in tech and AI innovation are defying expectations, the latest being Amazon, whose AI capabilities are fueling its next stage of growth. And it’s not just the chip makers and tech companies. It's businesses like Ali’s Chicken & Waffles restaurant in San Diego that can now serve twice as many customers as before through the use of ordering kiosks. Instead of replacing cashiers, the kiosks augment them, leading to better and higher-quality customer service, as well as improved capacity.

Optimists are banking on this kind of tech and AI innovation that can boost and accelerate productivity by multiples. Goldman Sachs believes that AI could have an even larger impact on the growth of US GDP than past innovations in electricity and personal computers. And with only 3.8% of businesses using AI, there’s a very, very long runway of economic potential. If, and that’s a big fat IF, all of that potential is realized, today’s lofty stock prices could look darn cheap in hindsight down the road.

To learn more about Ellevest and how we help our clients build their wealth with a values-aligned investment strategy, you can schedule a call with us here.

About Ellevest

Founded in 2014, Ellevest is a women-founded, women-led financial services company dedicated to closing the gender wealth gap. Our mission is to get more money in the hands of women, their families, and the next generation through personalized, intentional wealth management, and financial planning.